With the coronavirus crisis slowly coming under control, minds must now turn to the policies needed to get the economy back on track for full-employment growth.

The government and the central bank have come to the rescue of the economy with massive spending supported by the Reserve Bank of Australia’s (RBA) purchases of the government’s debt at near-zero interest rates.

“RBA governor, Philip Lowe, reminded the public in April of the need to reinvigorate the country’s growth and productivity agenda.”

But these supports for the economy come at a cost. Someone must pay the real cost of government services and transfer payments.

In the current low-inflation environment, a continuation of the present combination of fiscal and monetary policies would see that cost fall initially on savers who are inflicted with artificially low interest rates.

Over time, however, the cost would be shared across the wider economy, as low interest rates encouraged governments and business to invest in less productive, low-yielding assets.

It is then to the medium and longer term that we must now shift our focus.

Downside risks

That is why RBA governor, Philip Lowe, reminded the public in April of the need to reinvigorate the country’s growth and productivity agenda.

Lowe was just stating the increasingly obvious. In the US, the Federal Reserve has warned of lasting “medium-term” economic damage and its chairman, Jay Powell, has called on the White House and Congress to mobilise “the great fiscal power of the United States”.

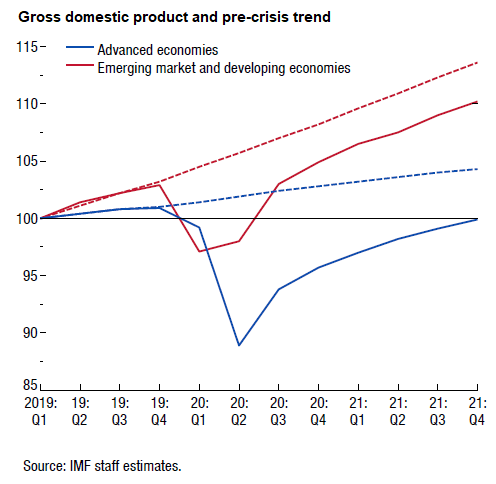

And, while the International Monetary Fund (IMF) has forecast a relatively short, sharp recession in Australia, it warns readers projections for the global economy come with dangerous downside risks.

“Much worse growth outcomes are possible and maybe even likely,” it says.

Many countries, it goes on to explain, are facing a multi-layered crisis comprising a health shock, domestic economic disruptions, plummeting external demand, capital flow reversals, and a collapse of commodity prices.

The emerging market and developing economies appear to be highly vulnerable. They have limited healthcare capacity, fragile governance and their economies are heavily reliant on skittish foreign portfolio investment and foreign debt.

Even excluding China, these countries account for about 40 per cent of global gross domestic product (GDP) growth.

Bad timing

Foreign investors are reported to have withdrawn a whopping $US95 billion from emerging markets since late January.

Since the disaster of the 1997 Asian financial crisis, when big currency depreciations left Asian governments and banks with crippling foreign-currency debts, emerging market economy governments have shifted to borrowing in their own currencies.

But, as the Bank of International Settlements (BIS) now explains, this shift has transferred unhedged currency risks to the foreign lenders whose market behaviour is now impacting on the borrowing costs of the emerging market economies.

The coronavirus crisis has struck at a bad time. The global economy was already struggling with productivity growth slowing, trade tensions rising and elevated debt levels adding to the risks.

Leading research institutions such as the Peterson Institute of International Economics and the Brookings Institution in Washington have been publishing scholarly warnings about the new challenges of prolonged low productivity growth.

According to the Brookings researchers, the world economy’s potential growth rate has slowed by around half a percentage point following the global financial crisis. The slowdown is widespread and could extend into the next decade, with the potential growth falling another 0.2 percentage points in the coming years.

Economists blame the pre-crisis global slowdown on weaker-than-average rates of capital accumulation, demographic trends and lower productivity growth. At the same time, Australian economists Warwick McKibbin and Adam Triggs have shown weak productivity growth has been linked to poorer fiscal outcomes, weaker export competitiveness, lower wages and higher income inequality.

Scarred economy

With little economic reform to show for the last 25 years, Australia has seen its multi-factor productivity growth collapse from an average 1.4 per cent a year in the 10 years to 2005, to just 0.4 per cent a year over the decade and a half to 2019.

Labour productivity growth, which plays a key role in wages growth, has almost halved from 2.7 per cent to 1.6 per cent a year over the same period.

With the early hopes for a post-crisis economic “snapback” overtaken by the severity of the economic damage in most economies, Australia’s economy almost certainly will suffer what the IMF calls “scarring”. Many good businesses will be wiped out and their workers tipped into prolonged unemployment.

Hence the increasing calls for the Australian government to formulate a plan to reinvigorate productivity growth.

Is economic reform politically feasible when a substantial proportion of the population is traumatised by the destruction of businesses, jobs and savings?

Perhaps not. But what is needed right now is a believable commitment by the federal government to restart the reform process.

The actual productivity gains from reform are likely to take years to materialise. However, a serious commitment to reform would be an instant signal to business that it could invest and rebuild in the expectation of stronger medium- and longer-term growth.

A commitment would also impose a useful discipline on the government itself.

Good policy

The immediate challenge in the face of the recession is to ensure there is no undermining of successful institutional bulwarks or retreating from the reforms inherited from the Hawke, Keating and Howard governments’ period of reform.

Fortunately, both the RBA and the government have drawn important lines in defence of good policy. Lowe has restricted the RBA’s bond buying to the secondary market.

“One of the underlying principles of Australia’s institutional arrangements is the separation of monetary and fiscal policy – that is, the central bank does not finance the government, instead the government finances itself in the market,” Lowe said in April.

“This principle has served the country well and I am confident that the Australian federal, state and territory governments will continue to be able to finance themselves in the market, as they should.”

Now Federal Treasurer Josh Frydenberg has come out against the new wave of protectionist pressure.

“While we must always safeguard our national interest, we must also recognise the great benefits that have accrued to Australia as a trading nation,” he said in a speech to the National Press Club.

“Unleashing the power of dynamic, innovative, and open markets must be central to the recovery, with the private sector leading job creation, not government.”

Of course, there will be a re-evaluation by industry of the risks and benefits of relying on global supply chains and no doubt there will be some expansion of domestic manufacturing. However, the test for whether a manufacturing project is viable in Australia must be its ability to survive without ongoing government assistance.

Proposed reforms

However, in addition to the legacy of 1980s and ‘90s reforms, there is a substantial body of potential reform that would impose relatively little adjustment cost on the hard-pressed public.

These reforms include raising the quality of government infrastructure investment and increasing the choice and quality of human services. Even the industrial relations reform proposed by the Productivity Commission back in 2015, and now urged on the government by the commission’s former chairman, Gary Banks, would be relatively costless.

And while tax reform has acquired a reputation for destroying political careers, the reforms proposed by the former Treasury secretary, Ken Henry, may be surprisingly well received.

Henry warns Australia’s dated tax system will not support the economic recovery and suggests replacing the goods and services tax (GST), payroll tax and stamp duty (all state revenue sources) with a national business cashflow tax.

The pandemic has reminded everyone of the importance of both maintaining well-funded essential government services and eschewing chronic deficit finance.

Governments need to run budget surpluses and reduce debt in the good times so they can come to the rescue of the economy in bad times.

The federal and state governments will emerge from this crisis with a lot of debt. And, while the immediate priority will be to get the economy going again, at some stage governments will have to start to wind back their debt.

The new National Cabinet may be exactly the right vehicle for building a national consensus in favour of reform.

The severity of the coronavirus crisis has created an extraordinary degree of policy plasticity.

With a spirit of compromise and the deft use of the incentives available within the federal-state financial relations, the Morrison government might be able to recruit the premiers as political partners in the bulk of the policies needed to repair the economy.

PH +61 427 448 634