COVID-19 lockdowns have severely hampered market activity across much of the nation this year, seeing many vendors postpone sales campaigns until buyers can attend auctions and open for inspections in person.

This has seen a significant reduction in the supply available to eager buyers, who have been forced to compete for the reduced purchasing opportunities, via online auctions or private sales.

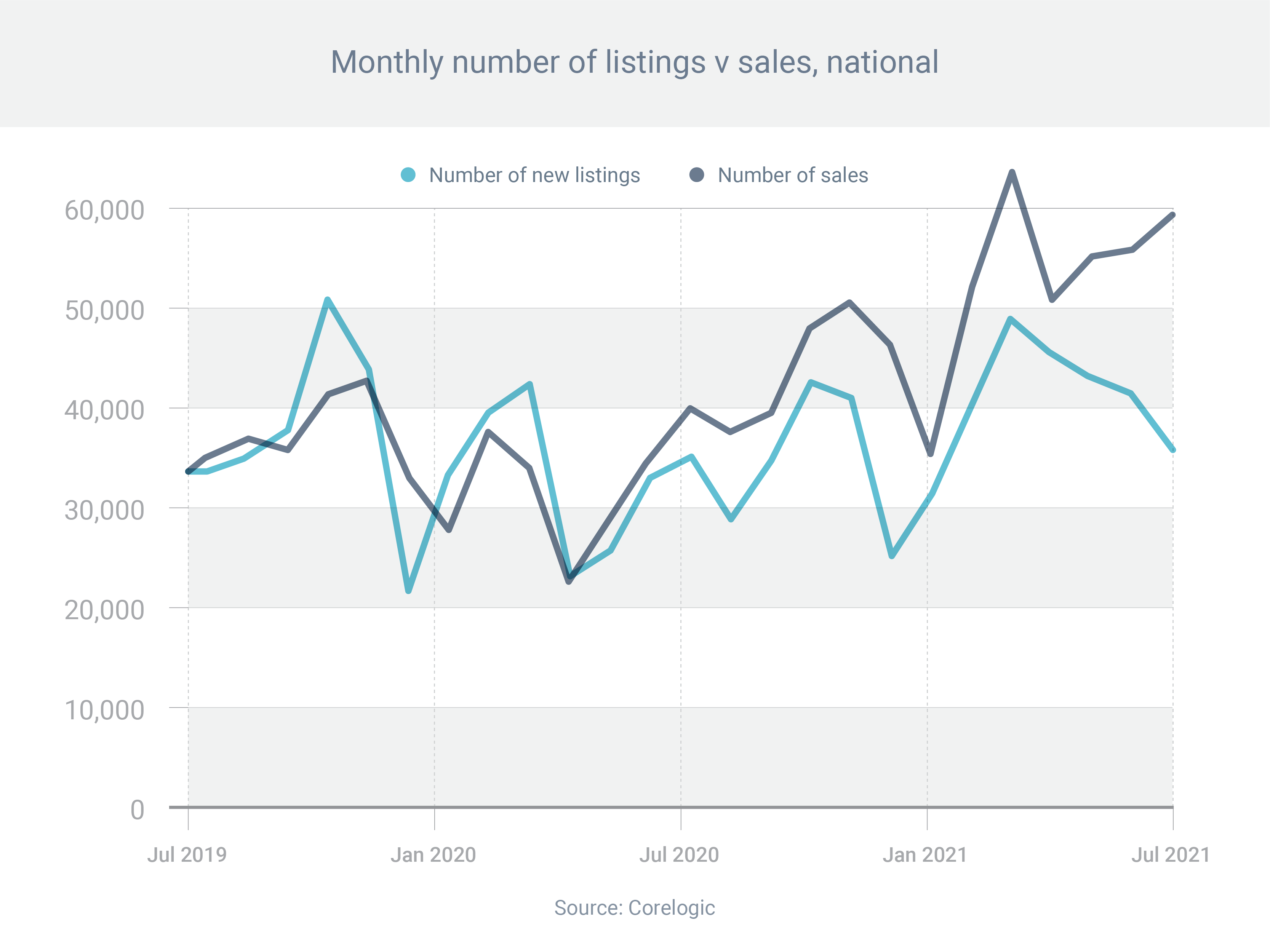

Across the nation, total stock advertised was down 27.1 per cent on the five year average in the four weeks leading up to August 8, according to CoreLogic.

Sydney, suffering under its protracted lockdown, has seen new listings fall more than 17 per cent over the four weeks leading up to mid August.

Once lockdowns eventually ease however, we can expect a surge in market activity, as vendors take the opportunity to hold in person auctions and open for inspections again.

This pattern was seen following Melbourne’s protracted lockdown in 2020 and subsequent lockdowns this year, which flowed on to drive uncharacteristically high auction numbers across Summer, and the busiest Autumn auction sales period on record.

However, despite the increased levels in supply, it’s likely to remain a sellers’ market across much of Australia.

So how should buyers navigate the purchasing process, amid surging demand and limited supply?

First off, they shouldn’t be disheartened. A buying campaign is usually a marathon, and prospective buyers accrue valuable knowledge of the market and their requirements along the way.

Patience is a vital quality. The temptation in this market is to compromise and buy something that isn’t quite right.

That only leads to buyer’s remorse down the track. Buyers need to trust that more supply will arrive in the future and remain discerning in the interim.

Saying that, if the right property presents itself today, a buyer should still know how to pounce.

That’s especially important amid the sporadic and uncertain nature of lockdowns.

Buyers who have carried out sufficient reconnaissance and due diligence between lockdowns, will be well poised to jump on unexpected opportunities that arise due to the disruption.

The challenge then becomes about paying a fair price. Typically, finding recent comparable sales are the key to establishing fair value.

Some investors are initially determined only to buy in a specific suburb or two, which makes them vulnerable when choice is low. Becoming enlightened about new ‘comparable’ suburbs reduces the risk of overpaying.

There are a couple of other factors to bear in mind, given the likely elongation of the buying process.

First, buyers should be mindful of the expiry date on their mortgage pre-approval. A three-month limit is not unusual, which is easily exceeded in today’s conditions.

Second, those who are looking to move home and trade properties in the usual order – sell first and buy second – may want to avoid short settlement periods to reduce the heightened risk of failing to find a replacement property and being forced to take up a short-term rental lease.

In these unstable times, it’s vital property investors are informed, prepared and agile – to ensure they lock in stable, long term returns.

PH +61 427 448 634