For first-home buyers locked out of the property market in far greater numbers than earlier generations, the possibility of property prices falling significantly is an enticing prospect.

Young buyers today are faced with property prices that soared during the Covid years when many of them were forced out of employment, lost work hours or saw their savings depreciate against rampant inflation.

Data released Thursday (20 October) by the Australian Bureau of Statistics has revealed that more than half (55 per cent) of Millennials (25–39 year olds) are homeowners compared with 62 per cent of Generation X and two thirds (66 per cent) of Baby Boomers when they were the same age.

Analysis of Census data from 1991, 2006 and 2021 showed that home ownership, including homes owned outright or with a mortgage, for those aged between 25–39 years has decreased in each successive generation.

The 25–39 year old Baby Boomers in 1991 were three times more likely than the 25–39 year old Millennials in 2021 to own their home outright.

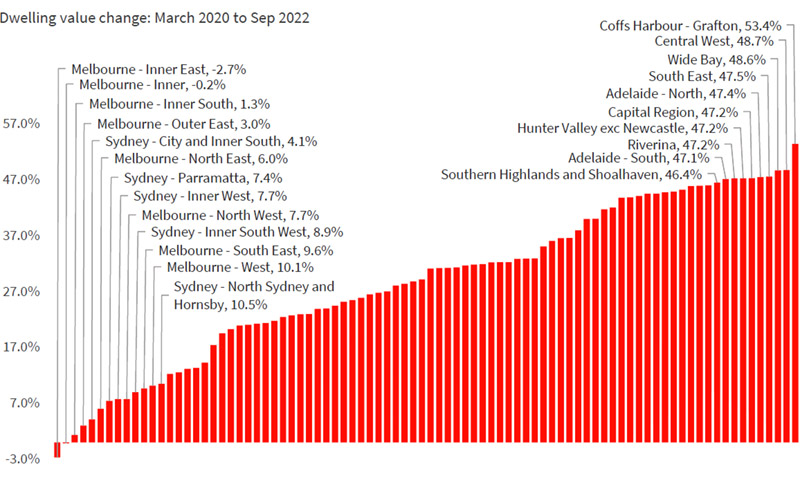

But with property values in decline in around four out of five Australian suburbs, young buyers who have managed to cobble together enough for a home deposit are timing their entry into the market.

Rapidly rising rents and record low vacancy rates are tempting them to buy, while falling property prices are serving as a strong deterrent.

So what will it take for the market to shed the capital gains achieved over the past few years?

Much depends on interest rates and what city or region you live in.

Source: CoreLogic.

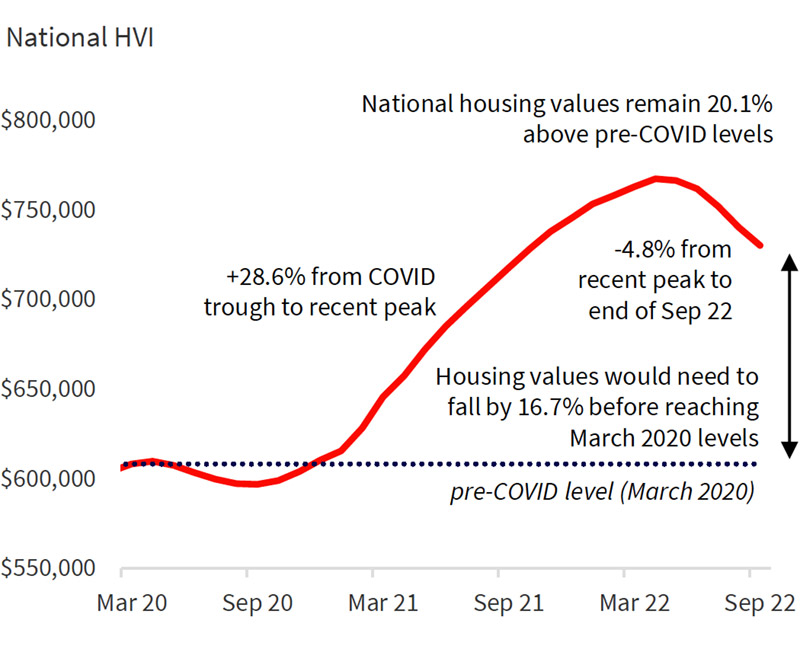

After CoreLogic’s national Home Value Index (HVI) surged nearly 29 per cent through the recent growth phase, the full extent of how far housing values will fall remains highly uncertain and largely dependent on the moves of the Reserve Bank of Australia over the next 12 or so months.

Since the national monthly HVI peaked in April, dwelling values are down 4.8 per cent to the end of September, ranging from a 9.0 per cent fall from peak in Sydney, to Darwin, where home values remain at a cyclical high.

Source: CoreLogic.

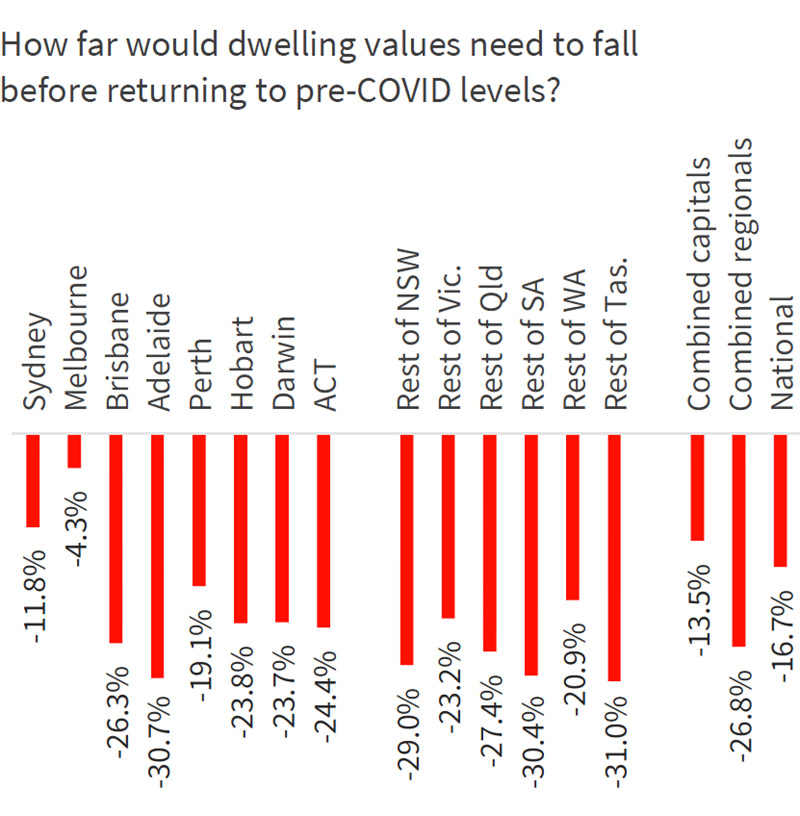

Mainstream forecasts for a peak to trough decline also vary remarkably, but generally range from around 15 per cent to 25 per cent across the combined capital cities.

First-home buyers, and others, trying to read the tea leaves and pick the bottom of the market

A 15 per cent drop from the peak in April 2022 would take CoreLogic’s combined capital cities index back to roughly March 2021 levels. A 20 per cent drop in values would see the index 2.2 per cent lower than the onset of the pandemic in March 2020. A 25 per cent drop in capital city dwelling values would take the index 8.3 per cent below March 2020 levels; a similar reading to August 2016.

Risks and opportunities vary

CoreLogic Research Director, Tim Lawless, said across the capital cities there were varying risks, and opportunities for first-home and other buyers.

“Arguably Melbourne’s housing market is most vulnerable; a further 4.3 per cent slide in dwelling values would take Australia’s second largest city back to March 2020 levels,” Mr Lawless said.

“This vulnerability isn’t due to housing prices falling faster than other cities, in fact Melbourne’s quarterly rate of decline, at -3.7 per cent through the September quarter, was a milder rate of decline compared with Sydney (-6.7 per cent), Brisbane (-4.3 per cent), Hobart (-4.5 per cent) and Canberra (-4.4 per cent).

“Melbourne simply didn’t see as much growth in values through the upswing, with a 17.3 per cent rise from the COVID trough to peak.

“This comparatively modest rise in values means Melbourne home values don’t need to fall as far as other capitals before wiping out all of its Covid gains.”

Source: CoreLogic.

At the other end of the spectrum, Adelaide’s housing values surged through the growth phase and, since peaking in July, have held reasonably firm.

“The market would need to drop by almost 31 per cent before values in the City of Churches returned to pre-pandemic levels,” Mr Lawless said.

Regional markets are also looking relatively secure from wiping out their Covid gains. The combined regionals index would need to see values fall a further 26.8 per cent before reaching March 2020 levels.

Comparing the generations

New analysis published by the ABS uses three Censuses to explore what was different and also what is the same for Baby Boomers, Generation X and Millennials. The ABS analysis compares the generations in terms of living arrangements, study, qualifications, participation in the labour force, working conditions, income and housing.

Duncan Young, General Manager, Census said, “Every dinner table in Australia has heard someone reflect on how things were different ‘back in my day’,” as he outlined the features of each generational grouping.

“Baby Boomers were born in the aftermath of the second World War and were young adults through Australia’s recession in the early 1990’s.

“In contrast, Generation X were born during a time when birth rates were lower in the late sixties and seventies. They entered early adulthood as Facebook launched.

“Millennials were born in the eighties and nineties and experienced early adulthood as smartphones and tablets became household items.”

The challenge faced by Millennials trying to enter the property market is greater than that which confronted earlier generations, despite them having higher education levels and fewer with the financial burden of parenting.

Millennials are the most qualified generation at 25–39 years of age with a greater proportion of Millennials having a non-school qualification—a certificate, diploma, or degree—than earlier generations. Over three quarters of Millennials (79 per cent) have a qualification compared with under two thirds of Generation X (64 per cent) and less than half of Baby Boomers (48 per cent).

Higher education qualifications were more likely for Millennials with 40 per cent having a bachelor degree or higher, compared with almost 25 per cent of Generation X. Only 12 per cent of Baby Boomers had a degree at the same age.

The ABS reported that participation in the labour force was similar for Millennials, Generation X and Baby Boomers, with around four in five employed or looking for work when they were 25–39 years old.

Over half (53 per cent) of Millennials have never been married, compared with 26 per cent of Baby Boomers at the same age.

The most common living arrangements for Millennials is living in a couple household with no children (36 per cent), which is twice the rate of Generation X (18 per cent) when they were 25–39 years old. One in five Millennials (21 per cent) are living with a partner and children, compared to more than half of Baby Boomers (52 per cent) at the same age.

PH +61 427 448 634