Throughout the last 12- 18 months, the construction market has grown more challenging with rising material costs and an unprecedented increase in delays, defects and deferred settlements.

An unfortunate consequence has been the rise of insolvencies across the sector.

Having access to up-to-date data to improve forecasting and time management has proved instrumental to the success of contractors and construction companies.

How can this data help businesses succeed?

1. Stay on top of market trends Having a good understanding of the current state of the construction market, including the cost of materials, labour rates, and current project information, can help you make more informed decisions and stay ahead of the competition. This information can also help you anticipate changes in the market and adjust your strategies accordingly.

2. Improve forecasting A clear understanding of project timelines is essential for building your pipeline. Knowing the expected start and completion dates for projects allows you to plan your workload and resources more effectively. This can help you take on the right projects at the right time, avoid scheduling conflicts, and ensure that you have the capacity to deliver projects successfully.

3. Reduce cost overruns with improved budget management By having access to up-to-date information on material and labour costs can ensure that your quotes accurately reflect the cost of a project and reduce the risk of unexpected expenses or cost overruns. This can also help better manage your budget and help ensure the project stays on track financially.

4. Better resource planning: Accurate forecasting also enables better resource planning and helps to ensure that the necessary resources, such as materials, equipment, and labour, are available when needed. This reduces the risk of delays and helps to ensure that the construction project is completed on time and to the required standards.

5. Improve Quality Control: A strong oversight of project timelines and pipeline allows for better quality control by providing construction teams with the resources they need, when they need them. This reduces the possibility of errors/defects and aids in the completion of the construction project to the required standards.

6. Identify new opportunities In a competitive construction market, it is important to stay ahead of the curve, know what your competitors are doing and where your next opportunity may lie. With access to up-to-date project data, you can identify new opportunities, build your pipeline and focus your efforts in areas where you can differentiate yourself from competitors.

Up-to-date project data and material costs are a valuable asset and can be used to your advantage to help: build your pipeline, produce more accurate quotes and improve forecasting to help keep to time and budget, even in challenging times.

Australian rent values have increased 24.1% between the start of an upswing in September 2020, through to February 2023. On the surface it would appears to be the perfect storm for property investors.

The pace of monthly rent increases is accelerating, the monthly vacancy rate nationally slipped back to 1.0% in February, and the count of rental listings on the market sank to around 96,000 over the past four weeks, down from a previous five-year average for this time of year of 150,000.

So, if rental income is rising and there is no shortage of potential tenants, why are investors shying away from the real estate market?

Investment purchases are declining

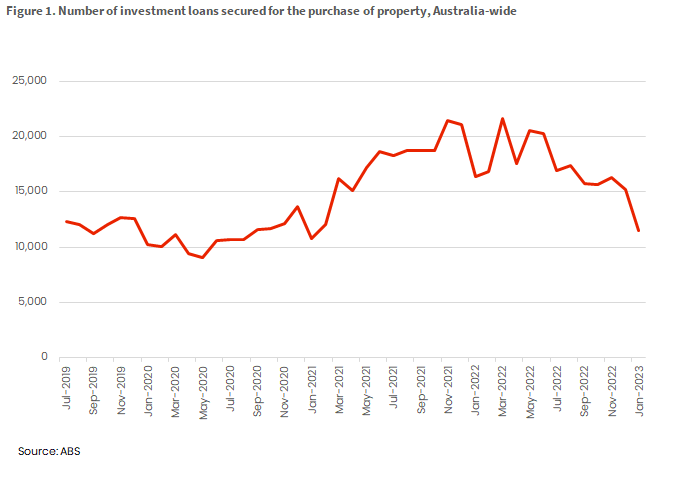

The number of investors buying dwellings has been falling since early 2022. Figure 1 shows the monthly number of loans secured for investment property purchases, which peaked at 21,663 in March 2022. As of January 2023, the volume of new investment loans had fallen around 47% to 11,485. The decline to January is compounded by a seasonal drop in sales, but the downward trend since March suggests waning investor interest in Australian real estate.

Rents rose at a record pace, but mortgage costs rose faster

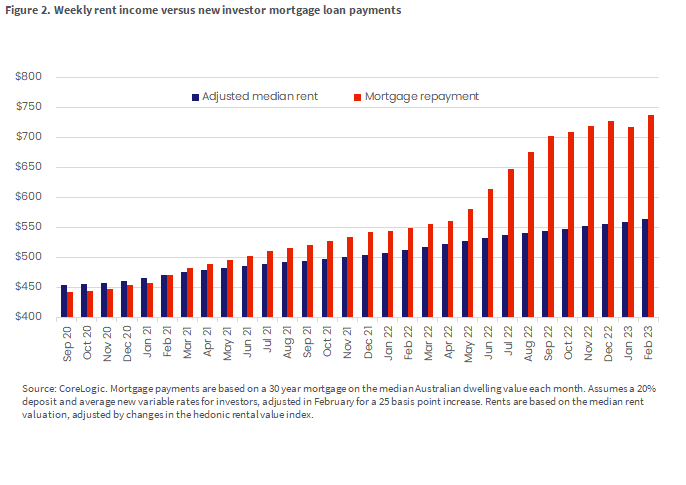

Since the start of a rental upswing in September 2020, mortgage payments for new investment mortgages have, on average, increased faster than rents.

Using Australia’s median dwelling value and rent as an example, weekly rent values have gone from $455 to $564 between September 2020 and February 2023. Weekly payments on a variable-rate investment loan on the median dwelling value rose from $443 to $738 per week (Figure 2). In this scenario, the difference between weekly rent and a new investment mortgage repayment has gone from $11 at September 2020, to -$174 by February 2023. On average, mortgage costs have risen much faster than rent values due to a record hike in the underlying cash rate, and dwelling values still being relatively high relative to where they were in September 2020.

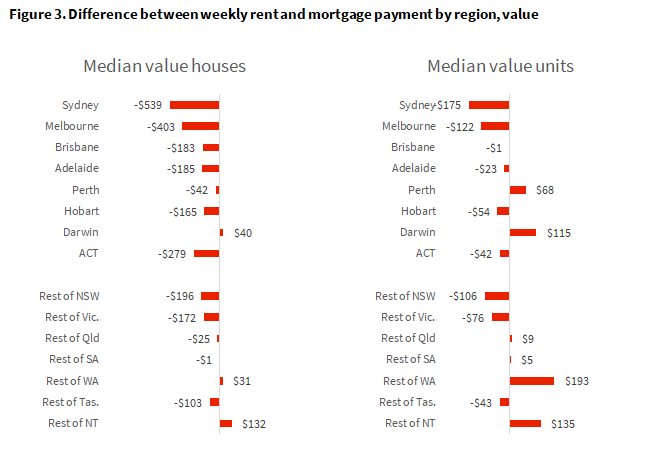

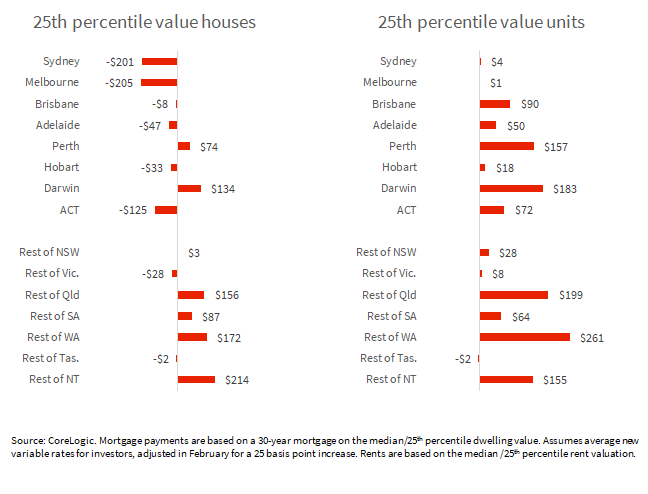

Figure 3 shows what the current difference would be between a weekly gross rent income and a weekly investor mortgage payment. These scenarios are presented for the median value in each region, as well as the 25th percentile valuation (a low home value). This is because investors generally target a lower-priced segment of the market, which tend to have greater yields.

Aside from resource-based markets (Perth and Darwin and parts of regional Australia), the value of mortgage repayments largely exceeds gross rental income as of 2023 for these price points. Even where there are marginal gains such as $4 per week at the 25th percentile unit value, this is only based on a gross estimate of rental income, and does not take into account maintenance, management fees or other additional costs associated with purchasing and owning an investment property.

Capital growth incentive is not what it used to be

Having high rent that exceeds mortgage costs is not the only reason investors take interest in property. In the 2019-20 financial year, ATO data suggests 53.7% of investment properties made a net rent loss. Negative gearing exists to help investors purchase real estate and provide rental housing when operational costs of the property exceed rental income.

In return however, investors expect capital gains. In the current environment opportunities for capital gains have been diminished by factors such as high interest rates and low consumer confidence. By the end of February 2023, Australian dwellings had seen a record fall of -9.1%.

Beyond the current market downswing, the RBA has flagged a broader shift in the Australian economy from the post-GFC era, in which low inflation and interest rates is less certain than it once was. This may mean that capital growth in Australian home values over the next decade may not replicate the 57% gains seen in the past ten years.

There are other changes to investment purchases over time that may have exacerbated the drop-off in investment purchases, and compounded losses on investment properties. These include a higher premium on mortgage rates relative to over-occupiers, changes to depreciation benefits in 2017, and greater protections and rights for renters through updates to tenancy law. It is worth noting however, that these longer-term changes to investment ownership over time did not dissuade an investment boom while interest rates were low. According to the ABS housing lending series going back to July 2002, investors secured a record $11.4 billion for the purchase of property in March last year.

Implications for renters

The reduction in new investment purchases exacerbates the issue of low rental supply and rising rents. As the proposition of individually-owned investment property in the market becomes less attractive, Australians need a new source of investment in rental accommodation.

This should at least in part be in the form of more social housing (or more funding for social and community housing providers), where increases in rent values tend to create the most vulnerability and insecurity across lower income households. This vacuum in the provision of rental accommodation has also seen more attention to the Build-to-Rent sector, which relies more on long-term rental income than capital gains. Greater accommodation of Build-to-Rent has already been seen in NSW, where the government announced a land tax discount to make these projects more viable.

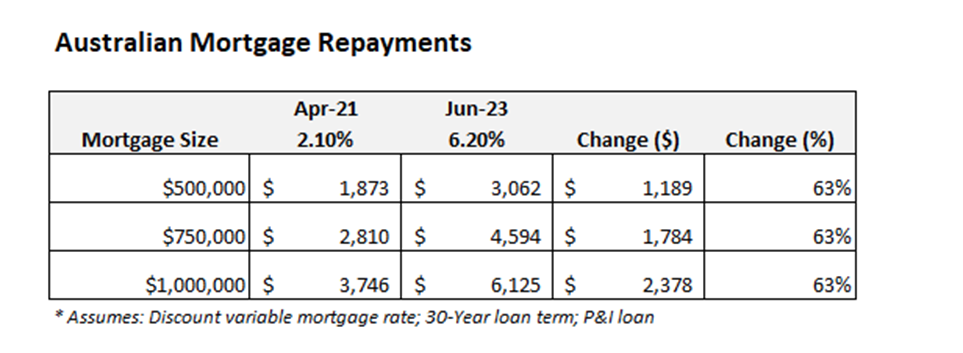

Hundreds of thousands of borrowers with fixed-rate mortgages face a bumpy road ahead this year as record-low fixed-rate loans expire and higher “revert” rates hit.

Banks are calling it a “fixed-rate cliff”, and the worst thing you can do is wait for it to happen.

There’s no need to panic; interest rates are simply returning to normal levels. However, if your fixed-rate loan is due to expire this year, your interest rate could potentially double.

One thing is for sure: your best move is to look at your options now and tackle the so-called fixed-rate cliff head-on.

Whether you break your loan term and refinance early or schedule loan settlement for when your current loan matures, there’s an opportunity right now to snag a better deal if you’re willing to invest a bit of time and effort.

The fixed-rate cliff

An estimated $29.8 billion worth of fixed-rate mortgages expired in 2022, and by the end of 2023, that number is forecast to total $158 billion.

The Commonwealth Bank (CBA) and Westpac alone have a total of $99 billion worth of mortgages coming off fixed rates in the second half of 2023.

Fixed-rate borrowers who secured loans at record-low pandemic rates need to get a handle on current interest rates to get a sense of what to expect.

RateCity predicts borrowers could be looking at revert rates of over 7 per cent if the Reserve Bank of Australia (RBA) cash rate increases another 1.25 percentage points to 3.85 per cent. Two of our biggest banks, Westpac and ANZ, expect this to happen.

The fixed-rate cliff affects a pool of around 500,000 borrowers, according to Canstar. They’ll feel the impact of all the rate hikes since May 2022, all in one go.

There have been nine cash rate increases and there are more coming. The RBA lifted the cash rate to a 10-year high of 3.35 per cent in February 2023, and RBA governor Philip Lowe confirmed that there are more increases to come, but said the RBA “is not on a preset course”.

CBA predicts we could see rate cuts start in November 2023; however, Westpac and ANZ don’t expect cuts until November 2024, and NAB doesn’t anticipate any cuts in the next two years, according to RateCity.

The average two-year fixed rate in 2020 was 2.46 per cent, and borrowers who roll off their fixed loan this month can expect an average variable rate of 5.43 per cent. That’s an increase of 2.9 per cent. On a $600,000 fixed-rate loan at 2.46 per cent, your current monthly repayments would be $2,680 (principal and interest). At 5.43 per cent, they’ll rise to $3,659 a month — that’s a $1,979 increase and is 37 per cent more*.

And that’s a massive jump overnight for the average household.

The honeymoon is about to end, and it’s all a bit of a shock, particularly for those who’ve never had to deal with interest rate rises. If you’ve had a mortgage for less than six years, that could be you.

But it’s not all doom and gloom for fixed-rate borrowers.

The silver lining

While borrowers with variable loans experienced the rate hikes bit by bit, fixed-loan borrowers have been protected. They’ve enjoyed record-low rates and some borrowers have really smashed down their loans. Congratulations if that’s you.

Some borrowers fixed their loans for five or more years at super-low rates. Lucky you if you still have a few years left on your fixed term — enjoy the hiatus.

Borrowers who’ve managed to save or who’ve been making extra payments off their loans are well down. You’ll fare better when your loan expires, but don’t be complacent.

The bottom line is, inflation and rising living costs affect us all and we’re all in this tricky economic time together.

The good news for borrowers is, while interest rates are rising, property prices and lending rates are falling, which means banks are in fierce competition for new business.

Fixed-rate mortgages hit a peak of 46 per cent of all new home loans in July and August of 2021, and banks are now trying to hold onto these customers and win more.

Now is an ideal time for borrowers with reverting fixed-rate loans to shop around for a better deal, rather than wait it out.

If you are on the precipice of the fixed-rate cliff, it’s a good time to rip off the band-aid, get professional advice and work out your game plan.

The pinch

The banks are worried, and for good reason. They’re nervous about their exposure when half a million borrowers’ repayments skyrocket, and they’re worried about the borrowers who’ll be hardest hit.

The RBA famously said it wouldn’t lift the cash rate until 2024, and borrowers made big life decisions with this in mind, like how much debt to take on, starting a family or business, or changing jobs.

Those who don’t have a lot of savings and live paycheck to paycheck are going to feel the pinch when their repayments jump.

Borrowers on one income, such as young families or those who get made redundant or who switch jobs with a pay reduction, will feel the pressure.

Small businesses or the self-employed, who are already dealing with rising business costs, could also feel it.

And it’s not just home owners who need to be on the alert.

Investors, particularly those who bought at the peak, need to keep an eye on their cash flow. They may have money now to cover things like repairs, insurance and strata bills, but they might have to dip into other cash reserves when they get hit with higher interest rates.

One thing is clear: refinancing is the best move for many borrowers on the cliff. The sooner fixed-rate borrowers look into their options and start to tighten the purse strings, the better off they’ll be.

The most vulnerable

Unfortunately, there’s a segment of borrowers who won’t be able to shop around for the best rate and will get stuck with their current banks.

Rising rates and falling property prices mean stricter bank stress tests, and some borrowers won’t have enough equity in their homes to refinance their existing loans. They’re effectively “trapped” when their rates revert.

If you’re one of the so-called “mortgage prisoners”, you need to a) find out as soon as possible and b) talk to professionals until you find a good solution.

Start with your lender or broker, and then talk to a financial counsellor if you need to.

Refinance

Thousands of borrowers on the fixed-rate cliff are already on the front foot and are refinancing in droves.

Refinance activity set a new record in August 2022, according to the Australian Bureau of Statistics (ABS), when almost $13 billion worth of owner-occupier mortgages were refinanced. That’s 17.5 per cent higher compared to August 2021.

Should you refinance? Start your research and find out.

Prepare now

When your fixed-rate loan expires this year, it’ll automatically revert to a variable loan with your current lender and your repayments will increase. This we know. So don’t wait and see, start a conversation with your bank or broker.

Talk to your mortgage broker

Ask your lender for their best rate. Banks have special retention pricing to help keep customers, so it’s a good idea to ask.

Also, find out what your loan-to-value ratio (LVR) is and if you can get a discount based on that. Hopefully, your equity has increased and you can get a better deal.

Don’t fear the break costs

Don’t let the thought of break costs stop you from refinancing early; there may not even be any break costs if you stay with the same lender when you move onto a higher rate.

And even if you switch lenders, the break costs for an early exit could well be lower than what you’ll pay in interest if you don’t exit your loan early.

Shop around

Find out what rates you can get elsewhere. Lenders are welcoming refinancers and will sharpen their pencils for borrowers switching banks. Also, look out for any cashback on offer as an incentive to switch your lender.

Be prepared to move with your feet if your lender won’t match a competitor’s rate. It does take effort to change lenders; however, banks have streamlined the process, and it’s likely worth your while to switch for a better rate.

Also, look at flexibility and think about how you might want to structure your loan.

Do you plan to make extra repayments? A split loan could be a good option — part fixed and part variable offers the best of both worlds. If you want the security of locking in your interest rate so you know how much your monthly repayments will be, then a fixed loan could be your best bet.

Look at your finances

Review your finances and get a really good picture of your financial situation. What are your incomings and outgoings?

Get a good handle on your budget and work out how much of a buffer you have — higher repayments need to come from somewhere.

Think ahead

Do you plan to have a family or sell anytime soon? Want to do renovations? Factor your plans for the future into your financial decisions now and make sure your loan offers the flexibility you’ll need when life changes.

Tighten the belt

I’m not going to talk about smashed “avo on toast”, but we have enjoyed several years of property prosperity. A few adjustments to your spending habits can help free up extra cash for your mortgage and every dollar counts.

Try an online spending tracker or app and you’ll start to see where your money goes and any “lifestyle creep” you may want to rein in.

Make extra repayments

Get into the habit of making additional loan payments now, or put the cash into a separate account that you don’t touch.

Rather than fearing the day your fixed-rate ends, adjust your budget now, while rates are still low, and see how much extra you can funnel into your mortgage.

You’ll soon build up a buffer for emergencies, and you’ll see how ready you are for higher interest rates. If you realise you’re not ready at all, you still have time to take action.

Don’t leave it too late

The best rates we’re going to see for a while are up for grabs right now and loan applications take time.

Give yourself time to get the best deal you can, even if it means scheduling your new loan settlement in the future. Your lender may allow you a “rate lock” for up to three months.

Yes, your bank will contact you about your loan expiration, but only with about six weeks’ notice. You’re better off contacting them now.

Stay focused

There’s a lot of noise out there from experts and no small amount of fear-mongering. The fixed-rate cliff is inevitable, yes, but you don’t have to fall off. Make an informed decision about your best course of action, put it in place and stay your course.

You can’t change inflation or control the Reserve Bank’s cash rate decisions, but you can focus on your own finances and get certainty for your financial future.

Now is the time to shift your money mindset, be proactive and take financial control.

Despite the ‘new normal’ of higher interest rates, 2023 will continue to offer valuable opportunities to real estate investors who are strategic in their property selection.

Property markets in trade exposed capitals, such as Darwin (pictured), Perth and Brisbane are well poised to return to a growth phase.

The relentless string of rate hikes kicked off by the Reserve Bank of Australia (RBA) in May last year has had a significant impact on a number of residential property markets across Australia.

However, despite economic headwinds, there are several key factors that continue to shape opportunities across some of our capital cities.

Here are the three drivers I believe will influence residential property investment opportunities in the year ahead.

The more affordable state capitals, in particular Perth, Adelaide and Darwin, outperformed the more expensive cities in 2022, and according to PropTrack (REA Group) data, Perth was the only state capital to have continued recording price gains in January 2023.

Residential property performance to 31 January 2023

Source: PropTrack Home Price Index 1 February 2023.

Affordability will be a critical factor this year as homebuyers and investors face the combined impact of higher rates and high inflation.

Higher interest rates don’t just affect a borrower’s repayments, they can also reduce borrowing capacity. The upshot is that many investors may look to more affordable markets, where their money stretches further and it’s possible to buy with a smaller loan.

The Real Estate Institute of Australia (REIA) monitors housing and rental affordability in all states and territories and publishes the results quarterly.

Here too, the more affordable states (notably the Northern Territory and Western Australia) stand out, with home loan repayments taking up around 31 per cent of income compared to as much as 51.6 per cent in New South Wales in the three months to September 2022. The Australian Capital Territory, despite its high median house price, is also relatively affordable due to the high average income of its residents.

Driver 2: Population growth

Population growth (particularly from migration) is a powerful driver of rental demand and rental price growth in the short to medium term. Most migrants rent when they first arrive in a new city.

The Federal Government has planned for 195,000 visa places this year, however China’s announcement that it will no longer recognise degrees obtained from foreign institutions online, meaning that students need to return to face-to-face learning, could considerably boost these numbers.

Most major centres around Australia are already experiencing extremely low vacancy rates. Data from CoreLogic and SQM research confirms that Perth has the nation’s lowest vacancy rate (0.5 per cent), while Adelaide and Hobart also have vacancy rates below 1 per cent. Population growth will continue to place pressure on the rental market and we will see increases in rental prices in most jurisdictions in 2023.

Rental market data – capital cities

City

Sydney

Melbourne

Brisbane

Perth

Adelaide

Canberra

Darwin

Hobart

Vacancy rate*

1.8%

1.7%

1.1%

0.5%

0.6%

1.9%

1.5%

0.6%

12-month increase in rents^

11.4%

9.6%

13.4%

12.9%

11.2%

4.3%

5.1%

5.3%

Gross rental yield**

3.2%

3.3%

4.3%

4.8%

4.0%

4.1%

6.3%

4.2%

Sources: *SQM Research as at December 2022. ^CoreLogic as at January 2023. **CoreLogic as at 1 February 2023.

Driver 3: The economy and job market

A healthy economy is good for residential property markets. Job opportunities are a key driver of population growth, while stronger wages and wage growth support greater resilience to interest rate rises.

On this front, several of our markets remain well-placed for 2023.

While interest rates dampen domestic economic activity, we have seen sustained growth in our exports, such that Australia now records substantial trade surpluses. Those states with a large trade exposure are also those most likely to be resilient to the slowdown in domestic demand.

WA, Queensland and the Northern Territory are our most trade-exposed markets, and most likely to benefit from the continued growth in exports.

National property market’s bottom line

In the early months of 2023, I believe we will continue to see our more expensive cities grapple with the impact of rising interest rates.

In the meantime, many investors will be turning their attention towards our more affordable markets, where the benefits of lower entry costs and tightening rental vacancies are driving attractive opportunities from both a yield and growth perspective.

Article Q&A

What are the top three factors driving the Australian real estate market in 2023?

The three drivers that Damian Collins, Managing Director, Momentum Wealth, believes will influence residential property investment opportunities in the year ahead are affordability; population growth; and the economy and jobs market.

Which three state or territory property markets offer the best investment potential?

Damian Collins, Managing Director, Momentum Wealth, argues that states or territories with a large trade exposure are the most likely to be resilient to the slowdown in domestic demand and therefore offer property investment potential, namely Western Australia, Queensland and the Northern Territory.

When will national property prices return to a growth phase?

Damian Collins, Managing Director, Momentum Wealth, predicts that with inflation anticipated to be nearing its peak, the major residential markets will bottom out within the first six to nine months of 2023.

For aspiring home owners in 2023, the Real Estate Institute of Western Australia (REIWA) recommended getting financially fit before embarking on a house-hunting journey.

The new year usually marks the start of taking on new goals, and for a significant portion of Aussies, turning the Great Australian Dream of owning a home into a reality is usually in the cards.

But before hitting the market, REIWA advised home buyers to get their finances as lean as possible in order to be in top shape before applying for a mortgage.

“Start prepping now, even if you aren’t thinking of buying until mid-year, that way you’ll be in top shape by the time you want to apply for a loan,” according to the institute.

REIWA outlined six ways aspiring property owners can get financially fit before house hunting.

1. Manage your expectations

The institute acknowledged that the Reserve Bank of Australia’s (RBA) monetary policy tightening — which was kicked off in May 2022 to fight surging inflation — has changed the finance game in the market for property buyers.

“Eight consecutive interest rate rises have changed the lending climate and reduced buyers’ borrowing capacity,” REIWA stated.

As of December, the country’s cash rate stood at 3.10 per cent — its highest level in a decade.

According to the institute, the rate hikes have significant financial implications for borrowers.

“For example, last year’s rate rises added about $800 per month to an average $500,000 mortgage. You may not be able to borrow as much as you could when interest rates were lower,” the institute said.

If you’re a borrower approved for a loan a couple of months ago, REIWA pointed out that the terms of your loan will need to be re-evaluated following any subsequent rate increases.

Additionally, lenders are legally required to appraise your loan with an interest rate buffer of 3 per cent when assessing a borrower’s ability to repay their mortgage.

“This means if you’re applying for a loan with a variable rate of 5 per cent, they will assess your ability to repay with an interest rate of 8 per cent. This reduces your borrowing capacity,” the institute said.

To help alleviate this hip-pocket pain, REIWA recommended looking at homes in lower price brackets, in different suburbs or different types of dwellings.

2. Reduce debt and consider the use of buy-now-pay-later services

REIWA noted reducing personal debt can help get your financial ducks in a row before buying a home.

“Any credit cards you have are considered potential debt, whether or not you use them wisely, and reduce your borrowing power further. Consider paying them off and closing the accounts or paying them down and reducing the limit,” the institute said.

REIWA also pointed out other lines of credit that aspiring home owners can take into consideration, such as the use of buy-now-pay-later services.

With two lenders — Macquarie and ING — announcing at the tail end of 2022 that they will now consider potential borrowers’ use of buy-now-pay-later service in loan applications, REIWA opined that other lenders might follow suit in the near term.

“This means you may need to declare your limit, current balance and monthly repayments when applying for a loan. Pay them off and cancel them if you can, and don’t use them in the lead-up to applying for a loan,” it said.

3. Give yourself time

Similar to preparing to run in a marathon, REIWA acknowledged getting your finances into shape takes time.

For example, lenders may require borrowers to have six months’ worth of genuine savings before greenlighting a mortgage application.

REIWA also warned home buyers not to be complacent even if they were given a lump sum for a deposit or receiving a windfall that significantly boosts their bank account, stating that this usually “isn’t enough” to convince banks to say yes to a loan.

“They will also want to review your bank statements for several months, so you’ll want to make sure they look their best,” the institute advised.

If you haven’t already, borrowers are advised to start saving for a deposit. While having 20 per cent is not a must, having a bigger financial war chest means having a lower debt.

4. Cut the extra financial ‘calories’

REIWA recommended borrowers to do a deep evaluation of their spending and see where they can cut back to help them be financially fit for a mortgage.

“Lenders will look at all of your expenditure, including Uber Eats and subscriptions to streaming services like Netflix and Binge. Expenditure on gambling apps will also be scrutinised,” the institute stated.

In the lead-up to buying a home, the real estate body advised ordering less takeaway and reducing the subscriptions. If your budget allows, you can resubscribe once you’ve settled on the property.

5. Give your credit score a health check

Credit scores play a major role when applying for a home loan.

With this, REIWA underlined the importance of having a healthy credit score, which can be achieved by paying bills on time and regularly paying down debt will help improve your credit score.

It also noted that bankruptcies, defaults, unpaid bills and multiple unsuccessful loan applications would lower it. Once you know your score, you can take steps to improve it if you need to.

6. Go see a broker

Finally, REIWA advised home buyers to speak with a real estate broker before looking at any properties, comparing them to “a personal trainer for your finances”.

Licensed brokers can help aspiring home owners review bank statements, spending and financial situation and provide an appropriate plan of action to improve your financial position before you apply for a loan.

They will also help you find the best lender for your circumstances, for example, if you need a low-doc loan or have a small deposit.

One industry expert has advised investors of her non-negotiable practices they must employ heading into the new year.

According to Anna Porter, the principal of Suburbanite, 2023 presents a year of opportunity for savvy property investors clever enough to capitalise on market conditions. Falling under her umbrella of rules are practices such as budgeting, buffering, diversifying, and researching.

She emphasised that budgeting is crucial as 2023 “is certainly not the year to fall victim to stretching yourself thin”.

“The changes to the interest rate environment have already made a dent in the budgets of households all over Australia. Set your budget from the start and ensure you’re leaving enough room to be able to counter any further rate rises or unexpected expenses,” Ms Porter said.

At the Reserve Bank of Australia’s (RBA) final meeting for 2022, it opted to raise the cash rate by 25 basis points to 3.10 per cent, marking the eighth consecutive monthly increase. As a result, many Australians have seen their budget tighten as mortgages rose in accordance with the RBA’s decisions.

“When buying in unknown times, you’ll want to buffer, especially as home owners stretched for cash opt to sell their homes quickly,” Ms Porter said.

She explained a rise in mortgagee in possession sales could coincide with a rise in defective homes for sale, with Ms Porter outlining, “you might be snatching a bargain, but there could be defects you didn’t see warning of, and you’ll need a buffer to address them.”

As for where the best location to buy in during 2023 is? Ms Porter believes the year ahead presents a perfect opportunity to purchase beyond your backyard.

“Diversification is key in 2023,” she said. “We know there is plenty of opportunity for investors if they know what to look for.”

“You can still get a great investment property in South Australia with less than $500,000. With this kind of investment, you can typically get an older house, under half an hour of [the] city or a townhouse or villa in closer proximity to the CBD.”

Her final rule for investors heading into the new year is to ensure investors complete their homework — especially around vacancy rates — and understand the numbers surrounding any prospective properties, no matter where they choose to invest.

“Speak to valuers and local agents to make sure the numbers stack up and cross reference this with your own research,” Ms Porter concluded.

PH +61 427 448 634