Booming property prices have pushed Australia’s household wealth to record levels, despite hundreds of thousands of people remaining unemployed.

Key points:

- Australia’s total household wealth hit a record high of $12 trillion in December

- The value of the country’s residential property soared by more than $450 billion in the last six months of 2020

- Treasury warns the unemployment rate could increase in coming months

The value of Australia’s residential property jumped by roughly $250 billion in the last three months of last year.

It followed an increase in property values of more than $200 billion in the September quarter.

According to the Australian Bureau of Statistics (ABS), the combination of rising property prices and a recovery on stock markets saw total household wealth grow by $501 billion in the December quarter — the largest quarterly growth since December 2009.

The recovery in stock markets in the last half of 2020 pushed the value of Australians’ superannuation reserves back above pre-pandemic levels.

Superannuation reserves increased by $166 billion in the December quarter and reserves have now fully recovered from the losses experienced in the March quarter of 2020.

Household wealth hits new record, despite recession

It means total household wealth in Australia ($12 trillion) and wealth per person ($467,709) are both sitting at record levels.

ABS officials said the Reserve Bank’s expansionary monetary policy and government support for the housing sector had driven the surge in wealth for property owners.

“The December quarter growth in household wealth was driven by rising residential property prices, reflecting record low interest rates, support through government programs such as the First Home Buyer and the HomeBuilder schemes, and pent up demand from buyers,” said Katherine Keenan, the Head of Finance and Wealth at the ABS.

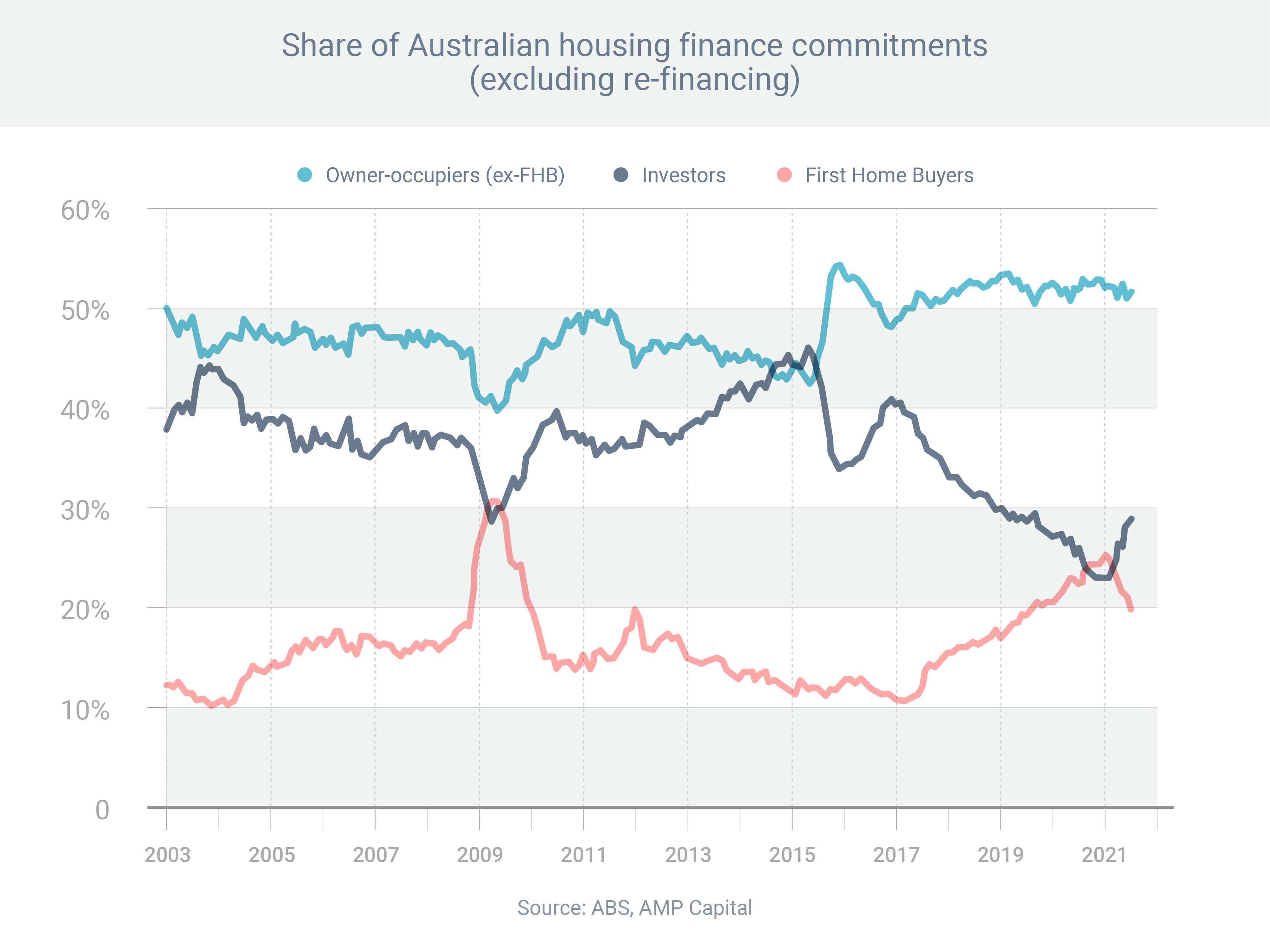

“The growth in residential assets was seen across both owner-occupier and investor housing in the December quarter.

“Owner-occupier housing loans grew 1.9 per cent, which was the strongest growth seen in four years, while investor housing loans grew 0.4 per cent, which was the first positive growth recorded in the past two years.”

ABS data also show that, despite the surge in property prices, the housing-debt-to-income ratio decreased from 139.2 to 139 in the December quarter, as growth in household income (1.2 per cent) was greater than housing debt (1 per cent).

The growth in income was driven by government income support packages implemented in response to the COVID-19 pandemic, including JobKeeper and the Coronavirus Supplement.

The housing-debt-to-income ratio has now fallen for the past 12 months, recording a 2.5 per cent fall through the year, which is the largest fall since 1990.

Concerns about property prices

Australian property prices returned to record highs in January, exceeding the peak reach in 2017.

The increase was broad-based, with every city and broader region recording a rise in prices.

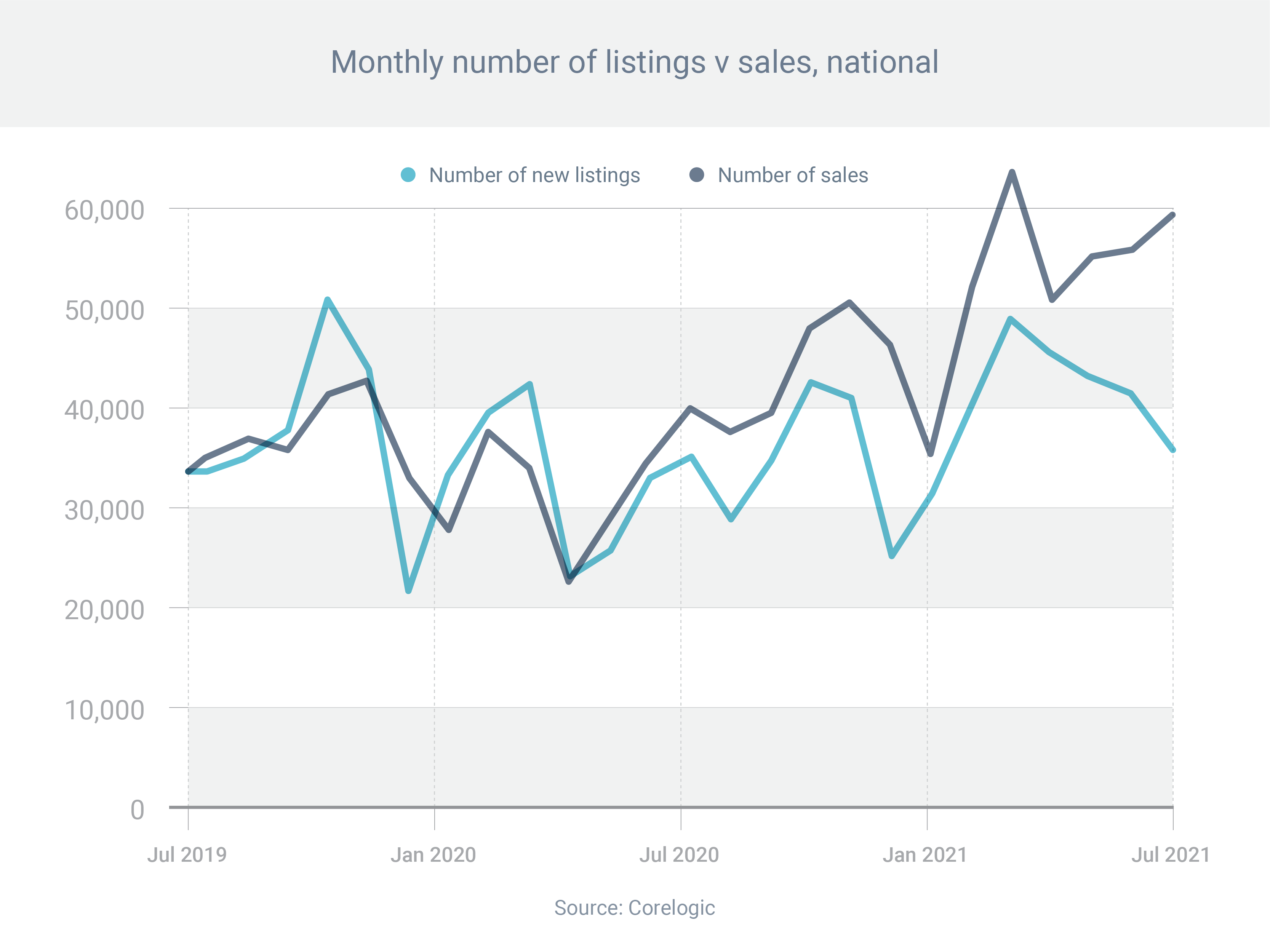

The next month, in February, house prices posted their sharpest monthly increase since August 2003, with analysts at CoreLogic saying the market was now entrenched in one of its strongest growth phases on record.

Eliza Owen, CoreLogic’s head Australian research, said few people were selling and there were lots of buyers scrambling for property.

“This is really a function of record-low mortgage rates, a very strong economic recovery and the fact that buyer demand is very strong against relatively low levels of stock,” she said.

“We’d either need to see some more restrained lending conditions or higher levels of supply to really start to ease the growth that we’re seeing in the housing market at the moment.”

This week, ANZ economists have significantly lifted their forecasts for house prices, saying they expected prices to rise by 17 per cent around the country this year.

House prices haven’t risen as much, nationally, since the late 1980s property boom.

Treasury warns unemployment rate could rise a little

The national unemployment rate is currently 5.8 per cent, having fallen from 6.3 per cent in January.

Officially, more than 805,000 Australians remain unemployed, down from one million in July.

Treasury officials have warned the unemployment rate could rise a little in coming months.

They say an extra 100,000 to 150,000 people could lose employment after the JobKeeper wage subsidy scheme ends this week, too.

“This does not mean that there will be a commensurate increase in unemployment,” Steven Kennedy, Secretary to the Federal Treasury, told senate estimates on Wednesday.

“Our view is that the adjustment away from JobKeeper will be manageable and that employment will continue to increase over the course of this year, although the unemployment rate could rise a little over coming months before resuming its downward trajectory.”

PH +61 427 448 634